These are the risks of the cash flood for the German start-up scene

A lot of money is currently flowing into German start-ups. This is not always a good thing, writes Bettina Engert.

The news about record investments is currently coming thick and fast. According to PitchBook, almost 80 billion euros flowed into Europe's start-ups last year in almost 8,000 financing rounds. Increasingly often from generalists with deep pockets such as the infamous Tiger Global or those from Silicon Valley. In Germany, too, start-ups are currently being showered with almost unlimited capital.

Why? Interest rates are still at a record low, inflation is rising and the digital and technology sector is currently the only area of the global economy that continues to grow and promises corresponding returns. More and more money is therefore flowing into venture capitalists, who in turn are competing to invest this money in the best ideas. Politicians praise the great conditions for founders and Germany as a location for innovation. But is that true?

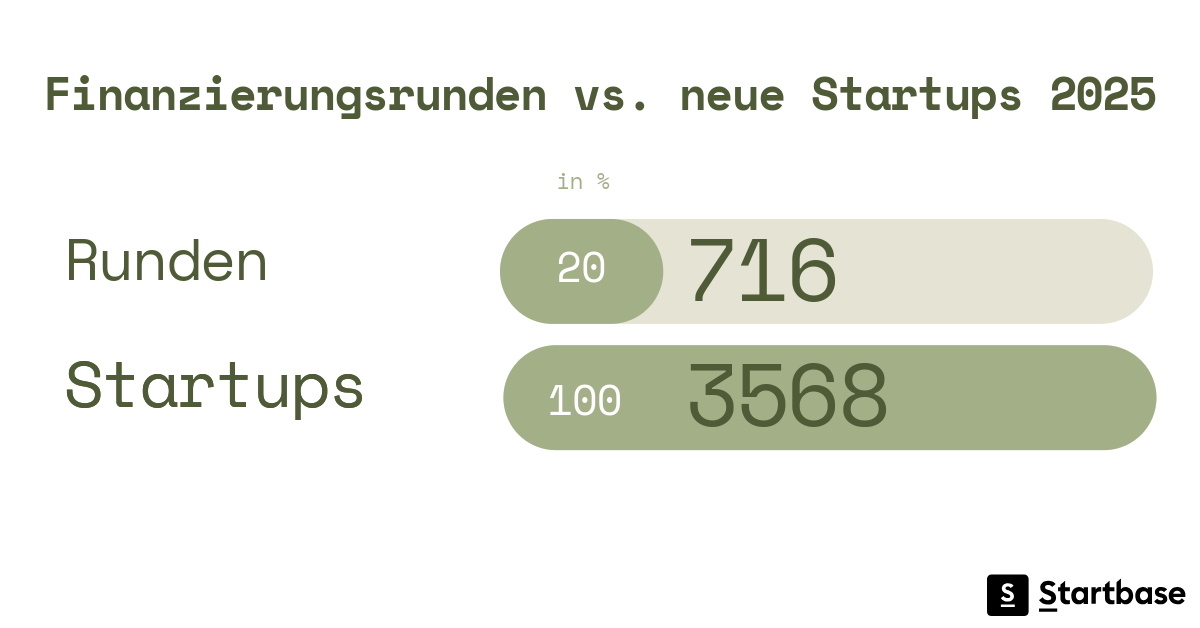

According to statistics, the number of VC-affine start-ups in Germany remains surprisingly constant despite countless funding programs and the reported record sums. This means that more and more money is flowing in, but despite the founder-friendly climate, this does not necessarily mean that more innovative companies are being created. A comparison with other countries also shows this in the high-tech sector: Germany's high-tech exports are stagnating, China has been outpacing the former inventor nation here for two decades. Many argue that there are structural problems and a lack of growth capital from Europe for the really big players, but is even more capital really the solution?

The disadvantages of "higher, faster, further"

The fact is that unicorns - i.e. private companies with rapid growth and a valuation of at least one billion - are currently growing faster than coronavirus variants. For comparison: in 2015, there were just 80 of these mythical creatures worldwide. In 2021, there were already over 1000, 26 of them in Germany, twice as many as in the previous year(Statista 2021). In the flood of records, when one potential unicorn follows another, it's easy to lose track. The same is true for some investors.

The competition for the best investments has created a new balance of power. Investors are now pitching to start-ups in order to be allowed to invest money. Founders like to put the timeline and VCs under pressure with absurd deadlines for the term sheet - i.e. the framework conditions offered. In order not to miss out on anything, VCs are making investment decisions faster and faster and sometimes completely remotely.

However, if the only principle that applies to financing rounds is "higher, faster, further", the quality of the due diligence, i.e. the heart-and-kidney examination of the business model, the market and the operating team, suffers. If it has to be done quickly, because otherwise another VC will get the chance, this is then simply outsourced to an external party.

The higher the round, the higher the "dilution"

The result: VCs know less and less about the companies in which they invest more and more money. Never met the founders and team? No matter, the main thing is to be there.

Conversely, this also applies to start-ups that opt exclusively for the backer with the deepest pockets and the highest valuation.

With the prospect of a windfall, it's easy to forget that the higher the round, the higher the "dilution", meaning that the founder loses more and more shares and therefore a say in their own company. Some people don't see a problem here - in the end, it doesn't matter who owns the thing on paper, as long as the idea is good - but similar to taking away piece by piece from your own home, the motivation to add a conservatory here also decreases, right? Especially in the early stages, the founder is usually the best owner. Experience shows that the more shares he/she loses, the less self-motivation there is to really drive the company forward.

Lack of substance and "natural selection" by the public market

Another disadvantage of the seemingly infinite availability of capital is that even highly loss-making business models without a unique selling point are promoted. These burn through a lot of money in the battle for market share at a very early stage and often lack a concrete plan as to how this should change after scaling. However, if the business model lacks substance, the hyped start-ups are then brought back down to earth quite hard at the IPO at the latest. In other words, natural selection on the public market - and alienated small investors.

The story goes that it was similar during the financial crisis in 2008 and the dotcom bubble in 1999. But these are just stories from veterans. After all, hardly any of the decision-makers - either on the founders' or investors' side - were of business age at the time.

Board meetings with approvingly nodding peers may be more relaxed - because criticism is rarely comfortable - but then there is also a lack of experience and the necessary overview when things aren't going so smoothly.

Like child stars in Hollywood - when start-ups lose focus

"So what?" The success-spoiled start-up on the financing wave is now saying to itself. Different times, no crash in sight, the local ecosystem has simply grown up. More start-ups mean more capital and consequently higher valuations. Besides, my idea is worth the money, many people think. But that's wrong.

As a result, some start-ups in the gold rush raise more capital far too early than they actually need. The maxim "a lot brings a lot" is then usually at the expense of healthy growth and the ability to innovate. Comparable to child stars in Hollywood who later sink into the drug swamp, start-ups quickly lose their focus, take short cuts when scaling up and take risks in the early stages that they are simply not yet up to as an organization. If there is also a lack of perspective for the long-term development of the company, the consequence is that many - initially good start-up ideas - are soon on the brink of extinction despite record funding.

The good news at the end

Of course, the current windfall also brings many advantages. The shift in power means that founders are no longer in the supplicant position. This means that VCs also have to think again about how they can create concrete and long-term value in the start-up process. There is also finally European capital for high-risk bets in the technology sector, i.e. future-oriented topics that investors in Germany and Europe would have given a wide berth to a few years ago (keyword Isar Aerospace, Lilium, Volocopter and co.).

It is now up to the start-up ecosystem to make the right use of this windfall. We have it in our own hands.

Newsletter

Startups, stories and stats from the German startup ecosystem straight to your inbox. Subscribe with 2 clicks. Noice.

LinkedIn ConnectFYI: English edition available

Hello my friend, have you been stranded on the German edition of Startbase? At least your browser tells us, that you do not speak German - so maybe you would like to switch to the English edition instead?

FYI: Deutsche Edition verfügbar

Hallo mein Freund, du befindest dich auf der Englischen Edition der Startbase und laut deinem Browser sprichst du eigentlich auch Deutsch. Magst du die Sprache wechseln?